The case for small credit unions: Why their survival matters

We seem to be entering yet another cycle—a season marked by headlines announcing yet another small credit union merging into a larger one. And it’s not just happening more frequently—it’s accelerating. The only real pause in this trend came during the height of the COVID-19 pandemic, a rare moment of stillness in an otherwise relentless wave of consolidation.

At first glance, these mergers might appear logical, even necessary. But beneath the surface lies a more troubling reality. With every small credit union that disappears, we lose more than just another institution—we lose the soul of the credit union movement. If this continues unchecked, we risk a future where only a few massive credit unions remain, and the core values and community-driven principles that built this industry from the ground up will be little more than a memory.

Why Should We Care?

There’s no denying that some mergers are justified. Strategic alignment, financial necessity, or leadership succession issues can make them the right choice in certain cases. But the sheer volume and speed of these consolidations demand reflection. The credit union industry—once proudly referred to as a “movement”—is becoming increasingly indistinguishable from the very commercial banking sector it was created to challenge.

And this transformation isn’t just cosmetic. Small credit unions serve an essential role in maintaining the balance and integrity of the system. They are our best argument for keeping the credit union tax exemption intact. When only massive institutions remain, the rationale for those tax benefits erodes under the weight of billion-dollar balance sheets and bank-like profit margins.

The Challenges Facing Small Credit Unions

We can’t ignore the very real hurdles small credit unions face. Staying competitive requires resources that many of them simply don’t have:

- Attracting and developing future leaders who are equipped to navigate an increasingly complex financial landscape.

- Competing in the digital marketing space where big budgets often determine visibility and member acquisition.

- Offering modern products and services that meet the expectations of today’s consumers.

- Finding skilled, affordable talent to operate in a digital-first, compliance-heavy world.

These aren’t insurmountable problems, but they are collective ones. The survival of small credit unions requires collaboration and support from the broader credit union ecosystem—especially the largest institutions, who once shared the same humble beginnings.

Remembering Our Roots

Credit unions were born from adversity. In 1934, in the depths of the Great Depression, they emerged as a radical solution to a broken banking system. They were founded on principles of cooperation, mutual aid, and financial self-determination. Back then, most credit unions were tiny—organized by communities, neighborhoods, or workplaces. They were run by members, for members, and operated as grassroots, democratic financial co-ops.

They weren’t built to compete with banks. They were built to serve people. To provide access to credit when no one else would. To create a safe haven for savings. To embody the belief that people helping people was not only a noble goal but a viable financial model.

Over time, as member needs changed, credit unions evolved too. Some of this evolution was necessary, even healthy. But in our drive to grow, many institutions began to look less like cooperatives and more like the banks we once set out to disrupt. Somewhere along the way, we began to prioritize expansion over purpose, margins over mission.

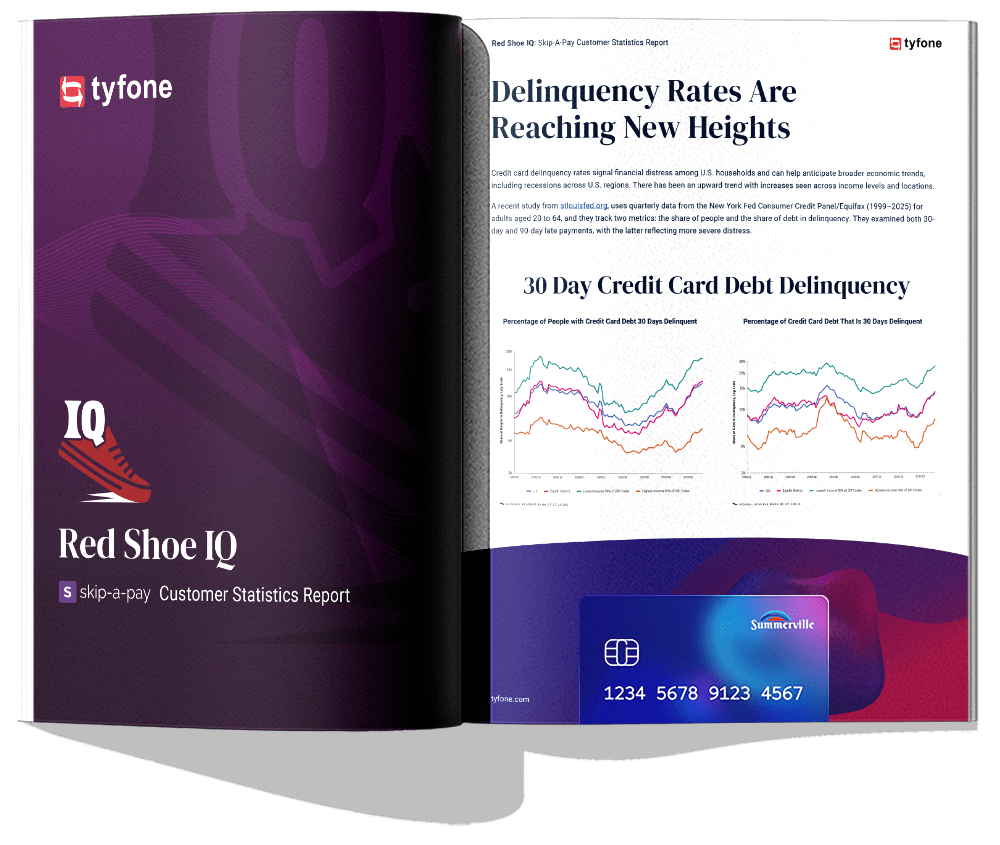

Story continued below…

FREE PAMPHLET

Red Shoe IQ:

Skip-A-Pay Customer Statistics Report

Inside this report you will find statistics on 30-day and 90-day debt delinquency across the U.S., comparison of loan skips and yearly revenue from loan skip fees across our customers, loan skips by institution asset size and number of members, and more!

What’s at Stake

Lost in the drive for size and scale are the small credit unions—many of which serve deeply rooted communities or specific fields of membership. These are not relics of the past—they are vibrant institutions providing essential services to people who might otherwise be underserved or ignored by larger financial players.

The cost of operating in today’s environment—technology, compliance, marketing, staffing—has made it increasingly difficult for these smaller institutions to keep up. But letting them disappear is not just a business decision; it’s an abandonment of our founding philosophy.

Meanwhile, many of the largest credit unions are posting profits that rival regional banks. While financial health is important, we must ask: at what cost are those numbers achieved? If we’re truly a movement, not a market, then we have a shared responsibility to preserve the diversity and humanity that small credit unions bring to the table.

What Must Be Done—A Call to Action

It’s time for the largest and most well-resourced credit unions to step up—not as benefactors, but as stewards of the very ecosystem that allowed them to thrive. Here are just a few actionable ways larger credit unions can support their smaller peers:

- Technology Infrastructure: Invest in a shared, state-of-the-art core processing system tailored to the needs and scale of small credit unions.

- Digital Platforms: Develop customizable mobile banking and online platforms that allow smaller institutions to offer modern services without bearing the full cost.

- Marketing Support: Create a cooperative marketing network that shares high-quality campaigns, creative resources, and digital expertise with smaller credit unions.

- Shared Services: Pool back-office functions like compliance, legal, IT, and accounting to help small credit unions manage operations more efficiently and affordably.

- Leadership Pipelines: Fund scholarship programs, internships, or fellowships focused on grooming the next generation of small credit union leaders.

These aren’t acts of charity—they are investments in the sustainability of the credit union model. Every large credit union operating today began as a small one. The future of our movement depends on honoring that journey and preserving the ladder that helped so many climb.

Conclusion: The Time is Now

Small credit unions are more than financial institutions. They are symbols of what makes credit unions unique. They serve niche communities with deep loyalty and personal connection. Their survival isn’t just a “nice to have”—it’s a must for the continued credibility and moral standing of our industry.

If we allow them to vanish, we don’t just lose branches or logos—we lose trust, purpose, and the foundational story we tell the public about who we are and why we matter.

So let’s not wait for another headline announcing the next merger. Let’s act. Let’s reach out, invest, support, and share. Let’s build a future where credit unions of all sizes can thrive—together.

Because in the end, we rise or fall not as competitors, but as a cooperative movement.

Based in Tucson, Arizona, Bergstrom Consulting Servicing provides CMO-level support to small and medium-sized credit unions across the U.S.

Disclaimer

The views, opinions, and perspectives expressed in articles and other content published on this website are those of the respective authors and do NOT necessarily reflect the views or official policies of Tyfone and affiliates. While we strive to provide a platform for open dialogue and a range of perspectives, we do NOT endorse or subscribe to any specific viewpoints presented by individual contributors. Readers are encouraged to consider these viewpoints as personal opinions and conduct their own research when forming conclusions. We welcome a rich exchange of ideas and invite op-ed contributions that foster thoughtful discussion.