What community FIs should do now with SaaS

SaaS may be necessary for many banks and credit unions to innovate faster and provide a better digital experience for their clients.

But, with rising regulatory scrutiny, partnership failures, and compliance gaps and data breaches, Saas requires disciplined due-diligence, a strong risk-management focus, and ongoing monitoring of all SaaS partnerships. Here’s what they should focus on going forward:

1. Reevaluate Your SaaS Strategy

FIs must now ask:

- Are we using SaaS to accelerate digital transformation, create strategic growth opportunities or just replace legacy software?

- Are we balancing speed of innovation with data governance and security?

- Where does it make sense to build your own vs. buy SaaS solutions?

- Modern SaaS can boost efficiency, but banks and credit unions must align each tool to business outcomes with an ROI focus.

2. Adopt a Security-First SaaS Architecture

SaaS platforms inherently come with data risks, third-party dependencies, and integration challenges. Community FIs should:

- Perform thorough security due diligence on all SaaS vendors.

- Ensure compliance with FFIEC, GLBA, SOC 2, and zero-trust policies.

- Centralize identity and access management across vendors.

- Invest in real-time monitoring and data leakage prevention.

Trusting SaaS vendors means verifying their operational and financial stability first—and continuously.

3. Treat SaaS Like a Strategic Enabler, Not Just an IT Expense

SaaS isn’t just a back-office tool—it’s a catalyst for transformation. Your institution should:

- Involve business and operations teams in SaaS selection.

- Use SaaS to rapidly test and launch new products or services.

- Ensure vendors provide API flexibility for custom integrations and efficiency.

- Track ROI and value delivered across each SaaS deployment.

If your SaaS tools aren’t creating measurable impact, they’re just overhead.

Story continued below…

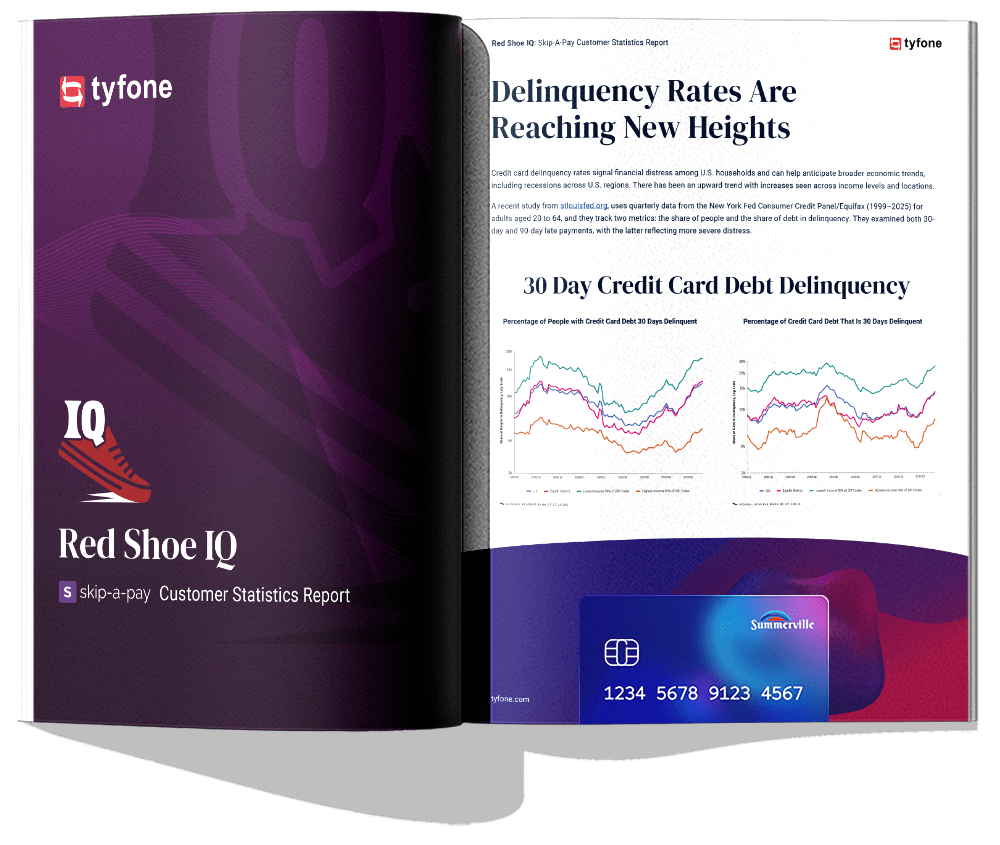

FREE PAMPHLET

Red Shoe IQ:

Skip-A-Pay Customer Statistics Report

Inside this report you will find statistics on 30-day and 90-day debt delinquency across the U.S., comparison of loan skips and yearly revenue from loan skip fees across our customers, loan skips by institution asset size and number of members, and more!

4. Select SaaS Partners Strategically, Not Just Conveniently

Don’t fall into the “shiny object” trap with flashy software tools. Look for:

- Vendors with deep financial services experience

- Strong implementation support, training, and configurability

- Transparent SLAs, roadmaps, and support models

- Deep compliance knowledge with clear compliance transparency

- Flexibility to grow with your needs (scalability and interoperability)

Think long-term. Your SaaS partner today may hold the keys to tomorrow’s digital infrastructure.

5. Prepare for Greater Vendor & Third-Party Oversight

Bank and credit union regulators are paying more attention to third-party risk, including SaaS vendors. Ensure your organization:

- Maintains a comprehensive vendor management program

- Monitors vendor risk post-implementation, not just at onboarding

- Documents how SaaS tools impact customer data, operational risk, and business continuity

The responsibility for vendor compliance doesn’t stop when the contract is signed.

6. Build a High-Value SaaS Stack

The most agile banks are creating an interoperable SaaS ecosystem—not relying on one-size-fits-all platforms. That means:

- Investing in integration capabilities and expertise to connect best-of-breed tools

- Leveraging low-code/no-code SaaS to empower operations teams

- Moving away from rigid core systems toward a flexible architecture

You don’t need one giant vendor—you need the right ecosystem.

In Closing…

SaaS is no longer just a tech convenience—it’s a strategic lever.

Banks and credit unions that embrace SaaS thoughtfully can accelerate innovation, control costs, and compete with fintech challengers. But success depends on governance, security, and alignment with real business needs.

Whether you’re modernizing operations or improving digital experiences, SaaS is not about tools—it’s about transformation.

Columbus, Ohio-based Visible Progress is a community bank and credit union consultancy helping financial institutions to create and implement strategies that bring daily, visible results.

Disclaimer

The views, opinions, and perspectives expressed in articles and other content published on this website are those of the respective authors and do NOT necessarily reflect the views or official policies of Tyfone and affiliates. While we strive to provide a platform for open dialogue and a range of perspectives, we do NOT endorse or subscribe to any specific viewpoints presented by individual contributors. Readers are encouraged to consider these viewpoints as personal opinions and conduct their own research when forming conclusions. We welcome a rich exchange of ideas and invite op-ed contributions that foster thoughtful discussion.