A 5-PART WHITEPAPER SERIES

Part 1: The aggregation trap.

How information services became commodities.

Part One of five, written for the boards and CEOs of community banks and credit unions. Outside companies are bringing together your consumers’ financial data, the largest AI companies are becoming the new front door to their finances, and new digital players are starting to sit between consumers and how money moves. This series explains what these changes can take away, what they cannot, and what to do about it.

By Dr. Siva Narendra, CEO & Co-Founder, Tyfone

Image generated by Gemini

Financial data has become a commodity.

For a long time, a community bank or credit union held an advantage that was easy to take for granted: it was the only one positioned to see and organize a consumer’s full financial picture. That advantage is gone.

Data aggregators, open-banking pressure, and a new generation of AI tools have turned basic financial information (balances, transactions, spending categories, the overall picture) into a commodity: something a consumer can now get more completely from an outsider than from any single institution, usually for free. This paper traces how that happened, shows what it looks like in practice through a firsthand test, and explains why the most tempting responses make the problem worse, not better.

The loss of the information advantage.

A consumer once typically had a single primary institution, and the more accounts they held there, the stronger the relationship became. That institution was the main window into their financial life, and keeping more of their money there reinforced its importance. This worked when most people’s finances were held across only two or three institutions. In that world, a primary bank could still show most of the consumer’s overall picture, and holding the majority of the relationship was itself an advantage.

That is no longer how consumers live. Checking may be at one bank, a credit card at another, a mortgage at a third, investments at a fourth, and retirement accounts somewhere else entirely. As finances spread across more providers, no single institution’s native app can present a complete financial picture on its own. And the budgeting and money-management tools many institutions added over the last decade have largely failed to become the center of consumers’ financial lives.

The failure of institution-built aggregation tools is not simply a matter of features; it is a matter of context. When consumers open their financial institution’s app, they usually have a specific task in mind: check a balance, pay a bill, transfer money. They are not necessarily looking to consolidate their entire financial lives at that moment.

Aggregation finished the job. Companies such as Plaid built the plumbing that pulls account data from thousands of institutions, normalizes it, and delivers it to whichever application the consumer chooses. Once consumers can move their financial data anywhere, no institution’s view is inherently special. The value shifts from holding the data to making sense of it. And while institutions can now aggregate external accounts, they still struggle to become the place where consumers choose to understand their financial lives. The challenge is no longer collecting data. It is earning the right to interpret it.

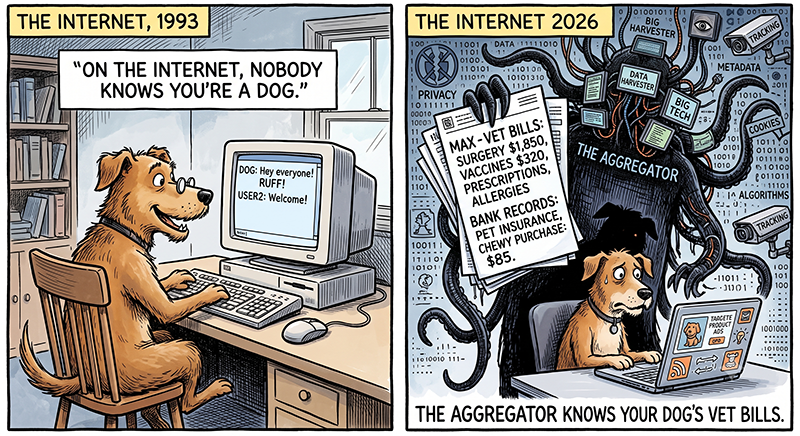

What total visibility looks like, firsthand.

This is easier to feel than to describe, so I tested it on my own finances. I connected my accounts to ChatGPT through Plaid: 28 accounts across eight institutions, covering checking, savings, investments, retirement, treasury holdings, and real estate. Linking every account and syncing full transaction detail took about 30 minutes, most of it running in the background while I completed other tasks.

An earlier generation of these connections, such as Perplexity’s first release, could pull little more than current balances. This time was very different. It pulled in full transaction history across every account and assembled a consolidated, categorized view of my financial life more complete than anything any one of my eight institutions has ever shown me.

That is the heart of the matter. None of the institutions in that set, including those where I hold my largest balances, could produce the same complete picture that a consumer tool assembled in roughly 30 minutes. What each institution still treats as a proprietary relationship asset is, from the consumer’s perspective, just one data feed among many.

What makes this more than a single-platform story is that the convergence is happening simultaneously across competing AI systems. Perplexity, which began as an internet search product and approaches financial data from a different angle than ChatGPT, has also integrated with Plaid. The two platforms are built differently and have different primary use cases, but both arrived at the same place: a neutral, AI-powered interface through which a consumer can consolidate and query their full financial picture.

The law is unclear; the trend is not.

It is tempting to attribute this shift to a single regulation. Boards should resist that instinct.

The CFPB finalized its Personal Financial Data Rights rule under Section 1033 of the Dodd-Frank Act in late 2024, signaling what looked like a clear mandate: consumers would have a formal right to use their financial data wherever they choose.

Since then, the picture has become less certain. A federal court has temporarily blocked the CFPB from enforcing the rule while it undergoes reconsideration. Compliance timelines have been paused, and an August 2025 notice reopened foundational questions, including whether institutions may charge for data access, a provision the original rule explicitly prohibited.

The lesson for boards is not that “the mandate is coming” or “the mandate is dead.” It is that the rule itself remains unsettled, while the underlying shift is already underway: consumers are increasingly able to take their data wherever they choose, driven by market forces rather than regulation alone. Strategy should follow that direction, not the specific outcome of the rule.

Story continued below…

FREE PAMPHLET

Youth banking: Growing the next generation of account holders.

Financial habits are formed early, but most financial tools are designed for adults. As a result, families often rely on cash, shared cards, or disconnected apps to teach money management, making it difficult to balance independence with oversight.

At the same time, younger generations expect intuitive digital experiences, creating a gap between how they interact with money and how financial services are delivered. Financial institutions need age-appropriate solutions that engage younger account holders while supporting parents and caregivers.

Where the money already went.

This is not theoretical, the deposits have already moved. Cornerstone Advisors estimates that more than $2 trillion has flowed from community banks and credit unions into fintech and high-yield platforms in recent years. Notably, roughly two-thirds of that movement came from Gen X and baby boomers, not the younger digital-native cohorts institutions often assume are driving the shift.

Cornerstone’s Ron Shevlin sums up the result in a phrase: the primary checking account has become a “paycheck motel,” a brief stop before the money moves on to wherever it is managed better. In the same research, more than half of younger consumers said they would switch to an institution that combined checking with the services they currently piece together elsewhere.

The mechanism is unbundling. When an institution cannot present a consumer’s full financial picture, the consumer assembles it themselves from specialists.

Each specialist then captures a slice of the relationship, and a slice of the balance sheet. Over time, the institution is left holding only the commodity layer: a temporary warehouse for payroll funds on their way to somewhere else.

The big-bank counterattack: charging tolls on the data.

The largest banks see the same trend and are responding where they have leverage: the data itself. In 2025, JPMorgan Chase moved to charge aggregators for access to consumer data, arguing it needed to recover the cost of secure infrastructure. By late 2025 it had signed paid-access deals with Plaid, Yodlee, Morningstar, and Akoya, the aggregators behind the overwhelming majority of third-party data requests on its accounts, with reporting putting Plaid’s potential cost in the hundreds of millions of dollars a year.

For a bank of JPMorgan’s size, this is rational, and it connects directly to the open fee question in the CFPB’s reconsideration. But it is a strategy available to the largest players, not to a $2 billion community bank or a regional credit union. For most institutions, the toll fight is happening overhead. It will reshape the cost of participating in open banking, but it is not a lever they can pull themselves.

What is more interesting is how the aggregation layer has adapted. Rather than resist these fees or fully pass them through to end users, Plaid appears to have absorbed much of the cost structure, preserving largely frictionless consumer access to aggregated financial data where it might otherwise have become metered.

That choice reflects a broader shift in where value is being created in the system. One way to understand it is that monetization is slowly moving away from charging for access to raw financial data, and toward the tools that sit on top of that data, especially AI-powered financial interfaces and agents that analyze and act on it.

In that world, large AI platforms don’t treat transaction-level data across thousands of institutions as a cost to reduce. They treat it as the basic input needed for their products to work. As that happens, the economics of the system naturally begin to shift toward meeting that demand.

Community institutions do not collect a toll in this arrangement. They are the source.

The no-win choice.

Here’s the problem, stated simply, because most responses to it make the situation worse, not better.

- If an institution opens up and shares data freely, it helps consumers pull everything together in third-party tools that often do a better job of showing the full picture.

- If it closes down and restricts access, it frustrates consumers, invites regulatory pressure, and still does not stop determined users from aggregating their data elsewhere.

That is the aggregation trap. Open or closed, both paths lead to the same outcome: the more an institution focuses on owning or interpreting consumer data, the faster that data becomes useful outside the institution instead of inside it.

As the earlier example shows, a free consumer tool can already produce a more complete financial picture than any single institution. In that context, spending time and capital trying to reclaim control over that view is less a strategy and more a losing position being defended.

What this means for your board.

The strategic mistake is to think the main battleground is information. That space now belongs to the largest banks and the big technology platforms.

A more useful question for a community institution is different: what can you do for a consumer that an aggregator, a data pipeline, or an AI model simply cannot do, even if it sees every account they have?

There are only a few real answers to that, and none of them are things that can be replicated remotely or through data alone. Those are what the next papers explore.

Part Two looks at how these forces move beyond data and into the consumer relationship itself. Part Three goes further, into payments and money in motion. Part Four examines what still holds. And Part Five brings everything together with what to do about it, starting from the first principle of the series.

The purpose of this paper is narrower, and it should be uncomfortable: the information advantage your institution was built on is gone, and most of the obvious ways to win it back will cost money and lose anyway. The sooner a board accepts that, the sooner it can stop defending the wrong hill.

About the author.

Dr. Siva Narendra is the CEO and Co-Founder of Tyfone, a leading digital banking technology provider serving community banks and credit unions across the United States. Over the past two decades, he has worked at the intersection of digital banking, payments, identity, and financial technology, helping institutions navigate periods of technological disruption while maintaining their competitive independence.

Sources

- CFPB, Personal Financial Data Rights rule (12 CFR Part 1033) and the 2025 Reconsideration Advance Notice of Proposed Rulemaking — consumerfinance.gov; Federal Register.

- Forcht Bank, N.A., et al. v. CFPB (E.D. Ky.), injunction against enforcement and stay of compliance dates, October 2025.

- Cornerstone Advisors, Stemming the Deposit Outflow and Beyond the Paycheck Motel, 2025 (Ron Shevlin).

- American Banker; Payments Dive; Bloomberg Law — JPMorgan Chase data-access fee agreements with Plaid, Yodlee, Morningstar, and Akoya, 2025.